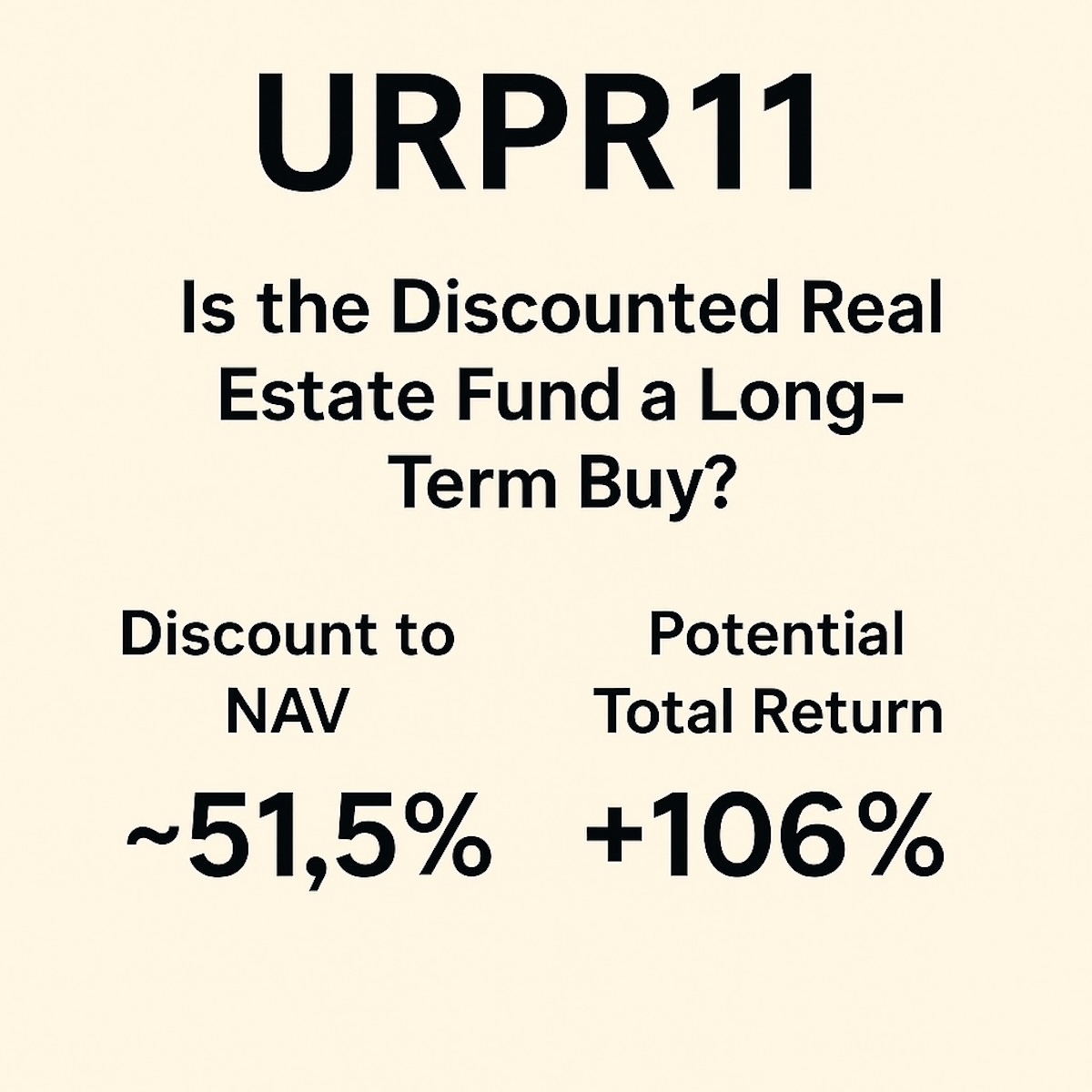

Ticker: URPR11 (Urca Prime Renda FII)

Current price: ~R$48.70

Net Asset Value (NAV): R$100.50

Discount to NAV: ~51.5%

Distribution Yield (last 12 months): Significantly reduced, recovering slowly

Sector: Real estate credit (CRI-backed development projects)

1. What Happened to URPR11?

URPR11 was once a high-yield real estate credit fund focused on structured debt for real estate developers in Brazil. In 2023, several projects funded by the FII entered financial distress, especially:

Prima Collection (RJ): Developer defaulted; assets being liquidated Anantara (RN): Suspended by city hall; legal proceedings ongoing Hotel Fasano Trancoso (BA): Construction halted due to environmental license suspension

As a result, the fund marked down a significant portion of its CRIs, leading to:

A sharp drop in NAV (from R$109.92 in 2023 to R$100.50 in May 2025) A suspension of regular monthly distributions Loss of market confidence, with the unit price collapsing to ~R$48

2. Is There a Recovery Plan?

Yes. The fund manager, Urca Capital Partners, has taken a proactive stance:

Legal enforcement: Dozens of lawsuits are underway to enforce guarantees and recover cash from delinquent projects Asset restructuring: Some projects, like Reserva São Francisco and Reserva São Francisco II, are being resumed under new ownership or terms Cash flow stabilization: The fund has recovered some cash from partial redemptions, e.g., R$10.5 million from one CRI in May 2025

The manager now projects that:

The NAV may gradually recover depending on successful litigation and project completion Monthly dividends may normalize over the next 12–24 months

3. What’s in the Portfolio Now?

| Project / CRI | Status | Value (May 2025) |

|---|---|---|

| Reserva São Francisco I & II | Restructured and progressing | R$36.7M + R$9.8M |

| Prima (RJ) | Liquidation in progress | R$16.5M |

| Hotel Fasano (Trancoso) | Legal injunction; valuation cut | R$15.7M |

| Anantara (RN) | Permit revoked; legal battle | R$12.1M |

| Other small CRIs | In recovery or performing | ~R$32M |

A portion of the portfolio (~25%) is in cash and liquid assets (LCIs, short-term fixed income), to maintain liquidity while recovery actions progress.

4. Why Is the Market Price So Low?

The fund trades at a steep discount (~51%) due to:

- Perception of high credit risk across multiple projects

- Suspension and uncertainty of dividends

- Loss of investor trust following multiple asset impairments

- Low liquidity and concentration in complex litigation outcomes

5. What’s the Opportunity?

Despite the challenges, the upside potential may appeal to long-term, risk-tolerant investors.

| Metric | Value |

|---|---|

| Market Price | R$48.70 |

| NAV (May 2025) | R$100.50 |

| Potential Gain to NAV | +106% |

| Targeted Yield (if normalized) | ~1.1%–1.3% monthly |

If the fund recovers part of its NAV and resumes dividends, even modestly, investors buying below R$50 may see:

- High double-digit annual returns, combining capital appreciation and dividends

- Potential price/NAV rerating if sentiment improves

6. Risks

- Legal risk: Lawsuits may drag on or result in unfavorable settlements

- Project risk: Delays, environmental restrictions, or further default

- Liquidity risk: URPR11 has low daily trading volume

- Market sentiment: Even if fundamentals improve, the market may be slow to reprice

7. How Does It Compare?

| Fund | Discount to NAV | Risk Profile | Monthly Yield |

|---|---|---|---|

| URPR11 | ~51% | High (recovery) | Low (temporary) |

| RECT11 | ~12% | Moderate | ~1% |

| RZAK11 | ~5% | Low | ~0.95% |

| HCTR11 | ~23% | High | ~1.2% |

URPR11 offers more upside than peers, but with substantially higher legal and credit risk.

8. Can Foreigners Invest?

Yes. Foreign investors and non-residents can invest in URPR11 under Brazil’s new simplified rules:

- No need for a legal representative for investments under R$2 million

- Most dividends from FIIs are tax-free for non-resident individuals

- No “come-cotas” taxation

- Must open a local investment account (through a Brazilian broker or bank) as a “non-resident investor”

Learn more about investing in Brazilian FIIs as a foreigner →

9. Final Thoughts

URPR11 is a distressed asset with asymmetric return potential. For long-term investors with high risk tolerance, it may present an opportunity to enter at depressed prices and benefit from:

- Asset recovery

- Gradual dividend normalization

- Potential NAV revaluation

However, patience is essential. Litigation, construction, and sentiment recovery may take 12 to 36 months. Diversification is critical — this is not a fund to concentrate in, but it could be a worthwhile small allocation for contrarian real estate investors.

📬 Follow Easy Brazil Investing for more English-language coverage of Brazil’s best investment opportunities. Or follow us on X

Read More: JHSF (JHSF3) Stock Analysis: High-Yield Exposure to Brazil’s Luxury Ecosystem

Leave a Reply